In a previous post, I mentioned that I need just over $3 million in order to achieve Financial Independence and maintain my current lifestyle. This equates to $7,000/month in today’s dollars at a 3.75% Safe Withdrawal Rate (SWR). This is a rate I feel will be able to sustain me for a long retirement as compared to the traditional 4% SWR, especially in this low interest rate environment.

XP – But how did I actually know my expenses would be about $7,000/month? By budgeting of course! Budgeting allows me to track my expenses so I know exactly where each dollar is going and allows me to make an accurate forecast of what I’ll need in retirement. It also allows me to identify unnecessary spending and identify areas that can be cut. If you don’t have a budget and rely on “mental accounting” to get you by, I’m afraid I have bad news: you won’t be able to achieve FI. At least, not easily since you’re just guessing and that’s no way to plan.

You won’t be able to achieve FIRE without a budget.

To start budgeting accurately, you’ll need to track where your money is going. You can certainly do this by hand or in an Excel spreadsheet, tracking and categorizing where every expense goes. But this is tedious. I highly recommend that you take advantage of tools that allow you to do this automatically. Two free tools to help you here would be Personal Capital or Mint. They allow you to link up your checking account & credit card accounts and pull in transactions automatically. Then it’s a trivial matter to build a budget off it. Yes, you do give up some privacy for this but I think it’s well worth it. Of course, you can pay for budgeting tools that may alleviate any privacy concerns you may have but for me, the free tools are fine. I would personally suggest Personal Capital over Mint as I’ve had issues with linking & syncing on Mint.

For most people, their expenses will naturally fall into several big categories: housing + associated expenses, utilities & recurring monthly bills, insurance (auto, life insurance, long term care insurance, and most importantly health insurance), food costs, and lastly other expenses. How you group these expenses is completely up to you. As a single person, I put food in the “Other” category and kept travel as a separate category altogether so I can easily track it. I would suggest these major categories and sub-categories:

| Main Category | Sub-Category |

| Housing | Mortgage or Rent Property Tax Homeowner’s or Renter’s Insurance Maintenance, HOA + other fees |

| Bills & Utilities | Electric & Gas Water & Sewer Fees Trash Fees Mobile Phone plan Cable & Internet Netflix + other streaming services |

| Insurance | Health Insurance Auto Insurance Life Insurance Long Term Care Insurance |

| Other | Travel Food/Groceries Auto Related Expenses Clothing Eating Out Entertainment Education Personal Care Other Services + Spending |

The main reason that I need a comparatively large nest egg is that I live in a High Cost of Living Area (HCOL) in San Diego, CA. According to Kiplinger in July 2020, San Diego is the 7th most expensive city in the United States, ahead of cities like Los Angeles, San Francisco, Boston & New York. You can argue with their methodology but I suspect they’re taking account not just raw cost but also income. San Diegans call this the “sunshine tax”. You’re going to pay to live here!

By far, the largest cost you’ll have to bear is housing cost. While San Diego is rated as the 7th most expensive city, in terms of median home price, it stands at 15th. According to Zillow, the median home price in San Diego, CA is $644,000 as of August 2020. That factors heavily into my budget. Housing prices have a direct influence on rent, so the more expensive houses are in a city, the more rent will be as well. My caution here is to make sure that you include all costs associated with owning a home if that’s your plan. Big ticket costs will be property taxes and maintenance. You’ll have these costs even if your mortgage is paid off.

Next would be your utilities and recurring monthly bills. Expenses in this section would include electricity & natural gas, water and sewer fees, mobile phone plan, cable & home internet, Netflix & other streaming services, and any other recurring expenses you think you’ll incur. Astute readers will note that my electricity & gas cost is low. The reason for this is that I have a paid for solar system that generates all the electricity I need.

Insurance would be my next major category. Within this, I only have auto insurance and health insurance. Others may wish to include life insurance and long term insurance as well. A note here on health insurance: as we’re part of the FIRE movement, there is a desire to retire early, whether it’s one year or one decade. If you do truly retire early without part time work that may provide health coverage, you’ll have to buy your own. Health insurance when purchased without any subsidy is expensive. Plan on paying at least $1,000 per person per month. This includes premium cost as well as out of pocket costs. Healthcare is broken in America and will only go up. It’s better to overestimate here than underestimate.

My next major category only has one item: travel. The reason for this is my desire to retire early so that I have the physical ability to be active and do what I’d like. One of these activities is to travel. It’s another category where you should not underestimate the cost. I’m budgeting $750/month or $9,000/year. That’s a lot but when you take a step back and realize that a trip to Europe can easily be $3,000 – $5,000, this will afford you 2-3 trips a year. Domestic traveling will be cheaper of course and you can hack your way to cheaper traveling, but it won’t be cheap. This is another area as you’re doing your own budget that can be cut down if can’t afford it. My expectation is that travel costs can be quite large the first 5-10 years of my own retirement and should then subside as I get the travel bug out of my system.

Last but not least is my catch-all category – Other. I did something here that may look odd: I put food/groceries in other. It works for me since I’m single, but for couples or those with dependents for one reason or another, groceries may be a big expense and may warrant its own main category. Aside from this caveat, other expenses that would go here include auto expenses (maintenance reserve + gasoline), clothing, eating out, entertainment, personal care, online services (cloud subscriptions for example), and any other expenses.

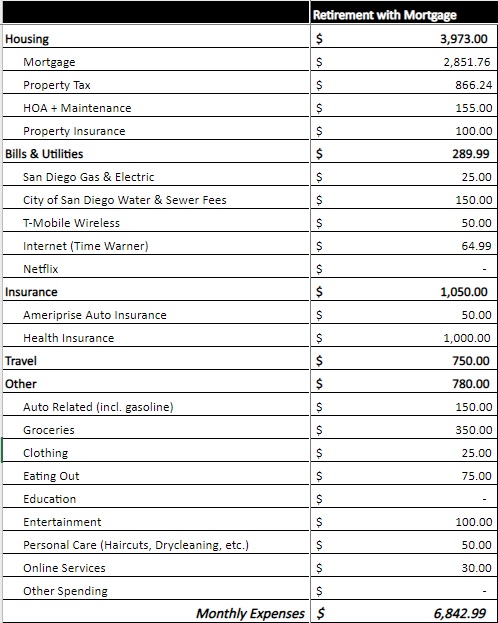

Here’s my actual budget based on carefully tracking my spending over many years and building an accurate budget off it. Only once you have an accurate picture of your expenses can you then calculate the nest egg that would generate the income need to cover these expenses.

Once you have a reasonable idea of what expenses you’ll incur in retirement, then you can go about calculating your nest egg. You’ll most often hear about the “4% Rule” or as I like to call it, the “4% Rule of Thumb”. This would suggest multiplying your annual expenses by 25 in order to get to be able to withdrawal 4% a year and hopefully have your money last your entire retirement. Some argue you can go higher and others say you should go lower to be safe. One of the biggest risks you can face once you’ve accumulated a nest egg and begin withdrawing from it is sequence of return risk. It basically says that if you’re unlucky enough, you’ll encounter a number of dramatically lower return years early in your retirement. This will make it very difficult to sustain that 4% withdrawal rate. But it’s a personal decision you’ll have to make yourself. I’ll write about it in detail at some point in the future. For me personally, I’m aiming for a 3.50% Safe Withdrawal Rate and that would require a 29 times multiplier. Here’s a table outlining some SWR and their multipliers. Just select the rate you’re comfortable with and multiply your annual expense by the multiplier:

| Safe Withdrawal Rate (SWR) | Nest Egg Multiplier |

| 5.00% | 20.0 x |

| 4.75% | 21.0 x |

| 4.50% | 22.2 x |

| 4.25% | 23.5 x |

| 4.00% | 25.0 x |

| 3.75% | 26.7 x |

| 3.50% | 28.6 x |

| 3.25% | 30.8 x |

| 3.00% | 33.3 x |

I hope that I’ve convinced you that you need a budget and have given you some ideas on how to go about it. If you’ve hesitated previously on establishing a budget, you should take the opportunity to set up one as an essential step on your FIRE journey. If you have any questions, feel free to drop me a note. Good luck!